TLDR: The Kelly Criterion turns a measured edge into a single number: the fraction of your account to risk on each trade so your capital compounds as fast as possible without going broke. This guide covers the formula, two worked crypto examples in the free Athenum Kelly calculator, why almost every professional bets a fraction of full Kelly, and when Kelly says to bet nothing at all. With Bitcoin near $64,000 on 2026-07-07, the bet size, not the entry, is what decides whether an edge survives a losing streak.

What is the Kelly Criterion and why does bet size decide your returns?

The Kelly Criterion is the mathematically optimal fraction of your bankroll to risk on a bet when you hold an edge. It was derived by John L. Kelly Jr. at Bell Labs in 1956, and Ed Thorp later used it to beat blackjack and run a market-neutral hedge fund for decades. It answers one precise question: given an edge, how much should you stake to grow wealth the fastest without courting ruin?

Bet size matters because returns compound. Two traders can take the exact same setups with the exact same win rate and still finish years apart, purely because one sized the bets well and the other did not. Stake too little and you leave growth on the table. Stake too much and an ordinary losing streak drops your account so far that the edge can no longer dig it out, since a 50% loss needs a 100% gain just to recover. Kelly maximizes the geometric (compounding) growth rate of the account rather than the average trade, and the geometric mean is what actually sets your terminal balance. It is the sizing layer on top of the wider risk-management framework: expected value and your expected-value calculator tell you a trade is worth taking, and Kelly tells you how large to make it.

How do you calculate the Kelly bet size?

For a simple bet with win probability p and net odds b (the profit per $1 risked on a win), the Kelly fraction is:

f = (p(b + 1) - 1) / b, which is the same as f = p - q/b, where q = 1 - p is the chance of losing.

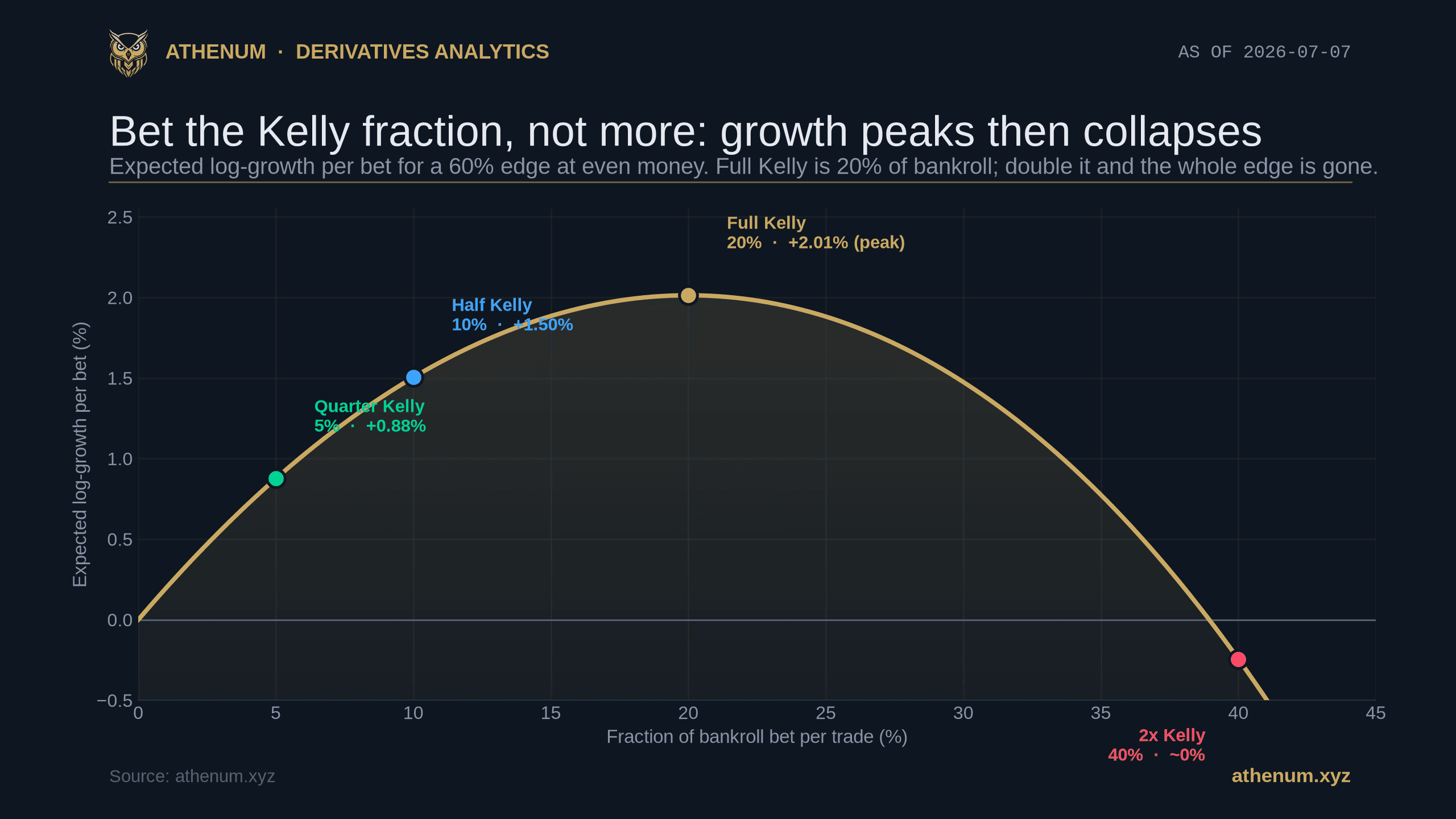

Take a clean example. Say a setup wins 60% of the time at even money (decimal odds 2.0, so b = 1) on a $10,000 account:

- f = (0.60 x 2 - 1) / 1 = 0.20, so full Kelly is 20% of the account, or $2,000. - The edge is +20%, half Kelly is 10% ($1,000), and quarter Kelly is 5% ($500).

The fraction scales with your edge, and it collapses to zero the instant the edge disappears. At even money a 50% win rate is a coin flip with no edge, so Kelly is 0%: do not bet. Below 50% Kelly turns negative, which means the correct size is zero (or you are on the wrong side of the trade).

The Kelly fraction is zero at a 50% win rate and rises with your edge: 60% wins maps to a 20% full-Kelly bet, 75% wins to 50%, at even-money odds of 2.0.

Win rate (even money) | Edge | Full Kelly | Half Kelly |

|---|---|---|---|

50% | 0% | 0% (no bet) | 0% |

55% | +10% | 10% | 5% |

60% | +20% | 20% | 10% |

66% | +32% | 32% | 16% |

75% | +50% | 50% | 25% |

You can run any of these numbers yourself in the free Kelly Criterion calculator, with no account and no sign-up.

What does Kelly look like for a real crypto trade?

Crypto trades are rarely even-money coin flips. You win or lose different amounts depending on where you exit, so the practical inputs are your historical win rate plus your average win and average loss. Kelly then becomes:

f = (W x avgWin - (1 - W) x avgLoss) / avgWin

Worked as a real system: a 45% win rate, an average win of $300, an average loss of $200 (a 1.5-to-1 payoff), on a $10,000 account:

- f = (0.45 x 300 - 0.55 x 200) / 300 = (135 - 110) / 300 = 8.33%, or $833.33 at full Kelly. - Half Kelly is 4.17% ($416.67) and quarter Kelly is 2.08% ($208.33). - The edge is $25 of expected value per trade, and the expected log-growth is 0.5146% per trade.

The free Athenum Kelly calculator on a 45% win rate with a 1.5-to-1 payoff: full Kelly 8.33% ($833.33), half Kelly 4.17% ($416.67), edge $25 per trade, expected growth 0.5146% per bet.

Notice that this system loses more often than it wins (45%), and Kelly still says to bet, because the winners are 1.5 times the losers. That is the whole point: edge, not win rate, drives position size. Your risk/reward ratio decides whether that edge exists in the first place, and Kelly decides how hard to press it once it does. Held perpetual positions also pay funding every 8 hours, so subtract that carrying cost from your average win before you trust the edge on longer holds.

Why do professional traders bet half Kelly, not full Kelly?

Full Kelly maximizes long-run growth, but it is brutally volatile. Drawdowns of 50% or more are normal at full Kelly even with a genuine edge, because the bet is large relative to the account. The saving grace is that the growth curve is nearly flat at its peak, so you can back a long way off and give up very little growth:

- Half Kelly keeps about 75% of the full-Kelly growth rate at roughly half the volatility. - Quarter Kelly keeps about 44% of the growth at a quarter of the volatility. - Overbetting is punished hard and asymmetrically. At twice the Kelly fraction the expected growth rate falls back to roughly zero, and beyond that it goes negative. Betting double Kelly is mathematically worse than betting half.

Fractional Kelly for a 60% edge: half Kelly keeps about 75% of the growth at 50% of the volatility, and quarter Kelly keeps about 44% at 25% of the volatility.

That asymmetry is exactly why the growth curve at the top of this post peaks and then rolls over. Leverage makes the trap sharper: a 100x perpetual position is an extreme form of overbetting, so size the leverage, not just the entry, and keep your effective bet at or below Kelly rather than above it. Most trading desks settle on half Kelly or less as a standing rule, precisely because it buys smoother equity curves for a small, known cost in growth.

When does the Kelly Criterion tell you not to bet?

Kelly goes to zero or negative whenever the edge is gone, and it is unforgiving about overconfidence:

- No edge, no bet. A 45% win rate at even money gives f = (0.45 x 2 - 1) / 1 = -10%, and the calculator prints "Don't Bet." A negative Kelly is the model telling you the odds do not pay for the risk. - Overestimating your edge is the classic path to ruin. If you assume a 60% win rate but the real number is 52%, full Kelly has you betting two to three times too much, and that overbet quietly turns a winning system into a losing one. - Kelly assumes independent bets. Crypto positions are often correlated, so five "separate" longs that all fall together are really one big bet, and your true risk is far higher than each per-trade Kelly implies. Crowded positioning is exactly when that correlation bites hardest.

The practical rules follow directly: estimate your edge from a large sample of trades, treat Kelly as a ceiling and never a floor, and when the edge is uncertain, bet a fraction of it and revisit as the sample grows.

The bottom line

A fixed 1% to 2% risk rule and your risk/reward ratio tell you whether a trade is worth taking; the Kelly Criterion tells you how large to make it once the edge is real. Bet the fraction, not the maximum, keep it at half Kelly or less when your edge is uncertain, and treat a negative Kelly as a hard no. Athenum aggregates live derivatives data across 14 exchanges and gives away 34 free trading calculators, with no account, no email, and no usage limits. Run your own numbers in the free Kelly Criterion calculator, then start a free 7-day Pro+ trial of the full Athenum terminal, no card required.

One terminal. All the data.

Liquidations, orderbook depth, whale walls & open interest from 4 exchanges, all real-time, in one place.

No credit card required