Blog

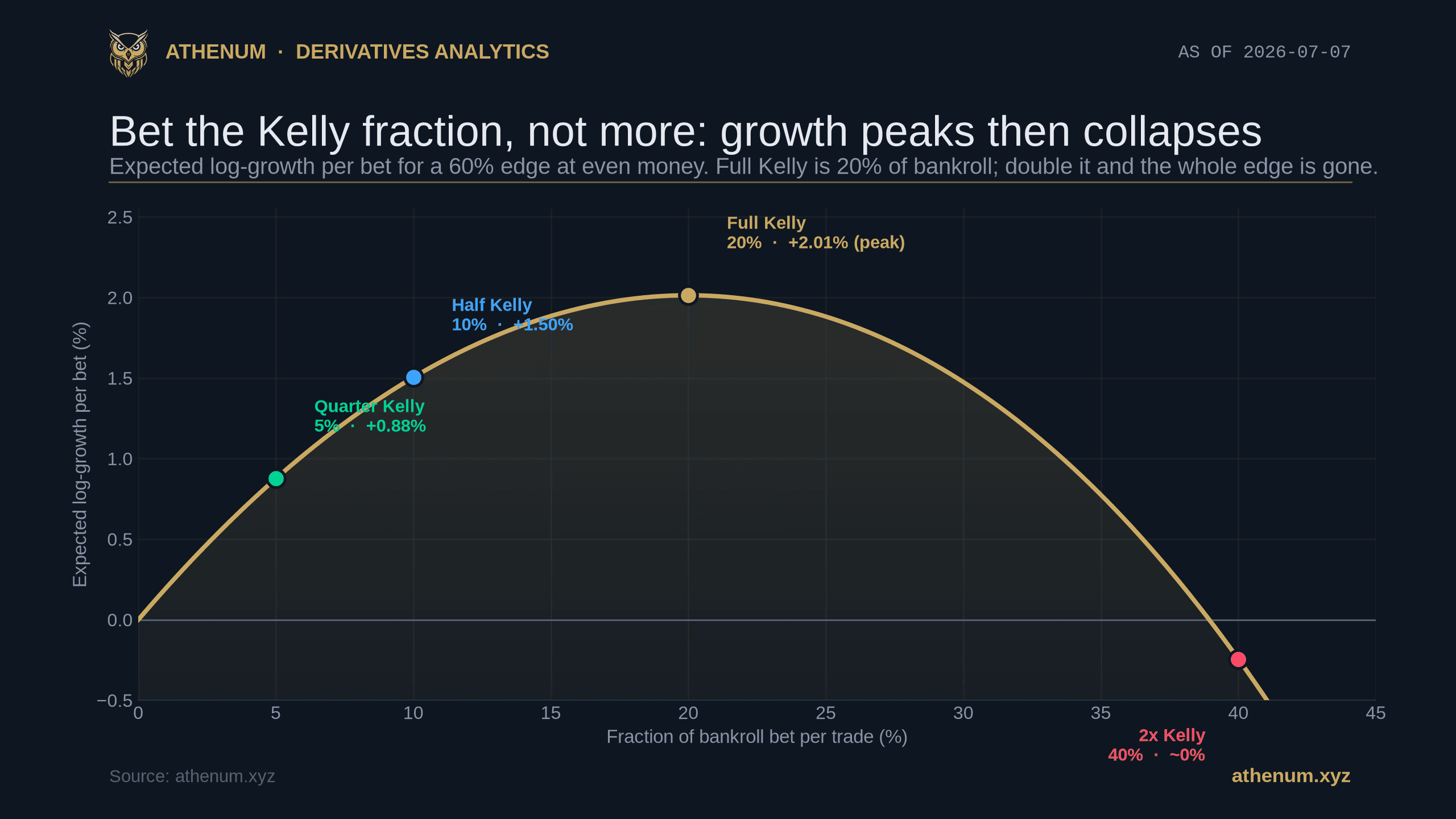

The Kelly Criterion for Crypto Position Sizing: How Big Should Each Trade Be?

The Kelly Criterion sets your optimal bet size from your win rate and payoff. Two worked crypto examples in the free Athenum calculator, plus why professionals bet half Kelly.

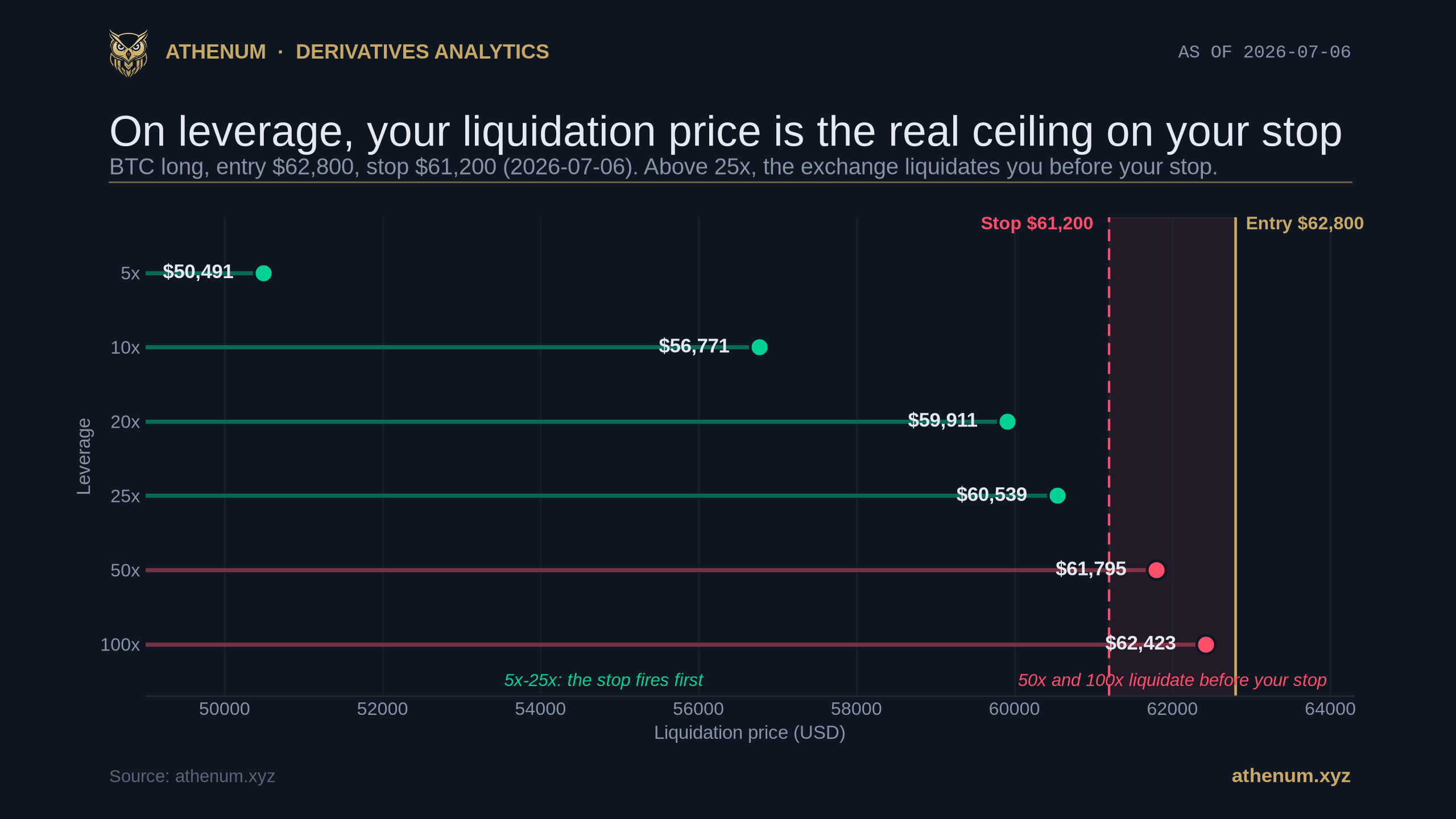

Risk/Reward Ratio in Crypto: How to Size a Leveraged Trade Around Your Liquidation Price

Your risk/reward ratio sets the win rate your system needs, and on leverage it also caps how wide your stop can be. A worked Bitcoin example with the free Athenum calculators.

The Perp-to-Spot Volume Ratio: Is a Crypto Rally Leveraged or Real?

The perp-to-spot volume ratio compares perpetual turnover to spot volume. Learn to read it, what a normal ratio is, and if a crypto rally is leveraged or real.

What Are Perpetual Futures? How Crypto Perps Stay Pinned to Spot

What are perpetual futures? Crypto contracts that never expire, held to spot by an 8 hour funding payment. How perps work, why funding exists, what they cost.

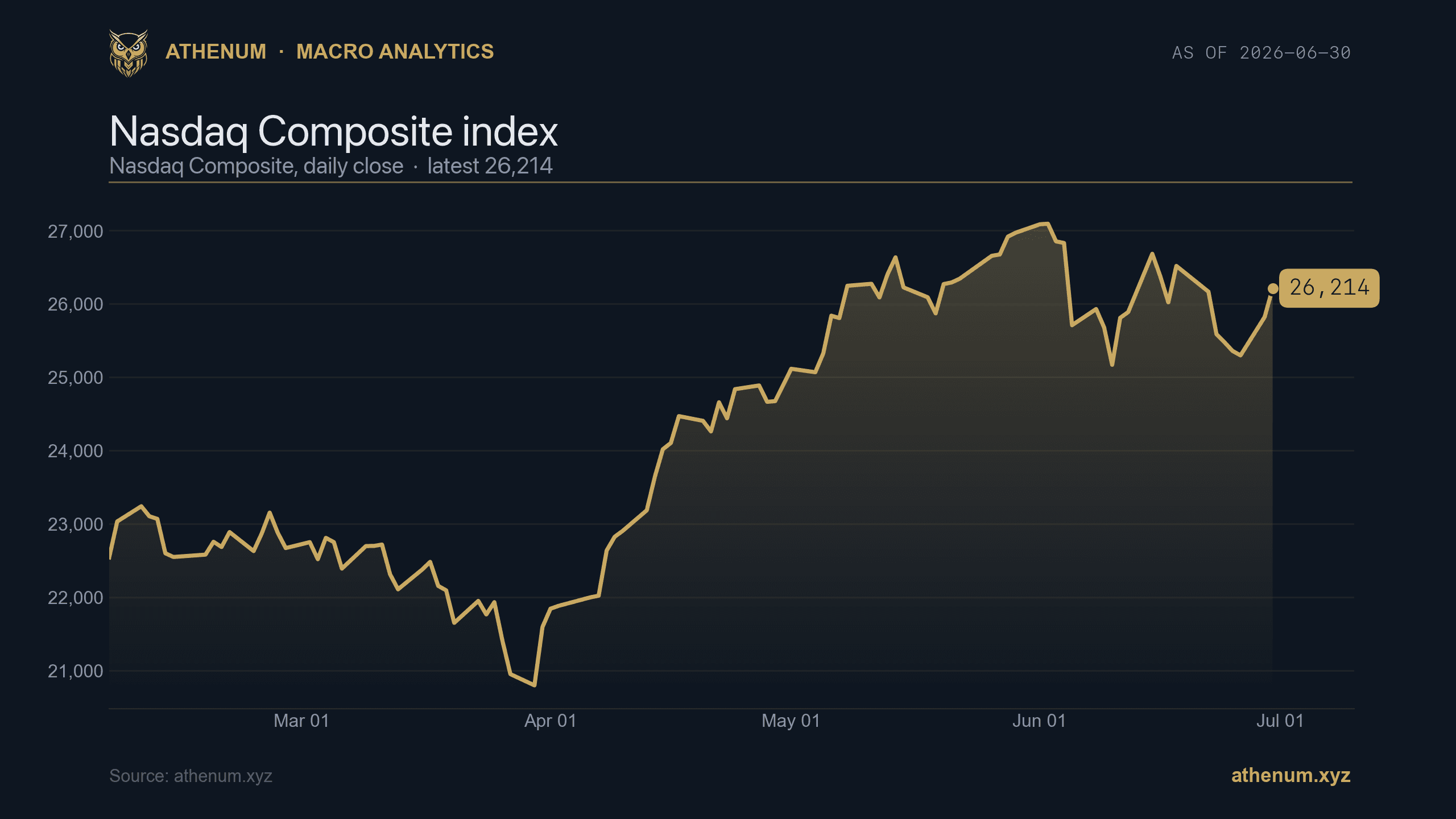

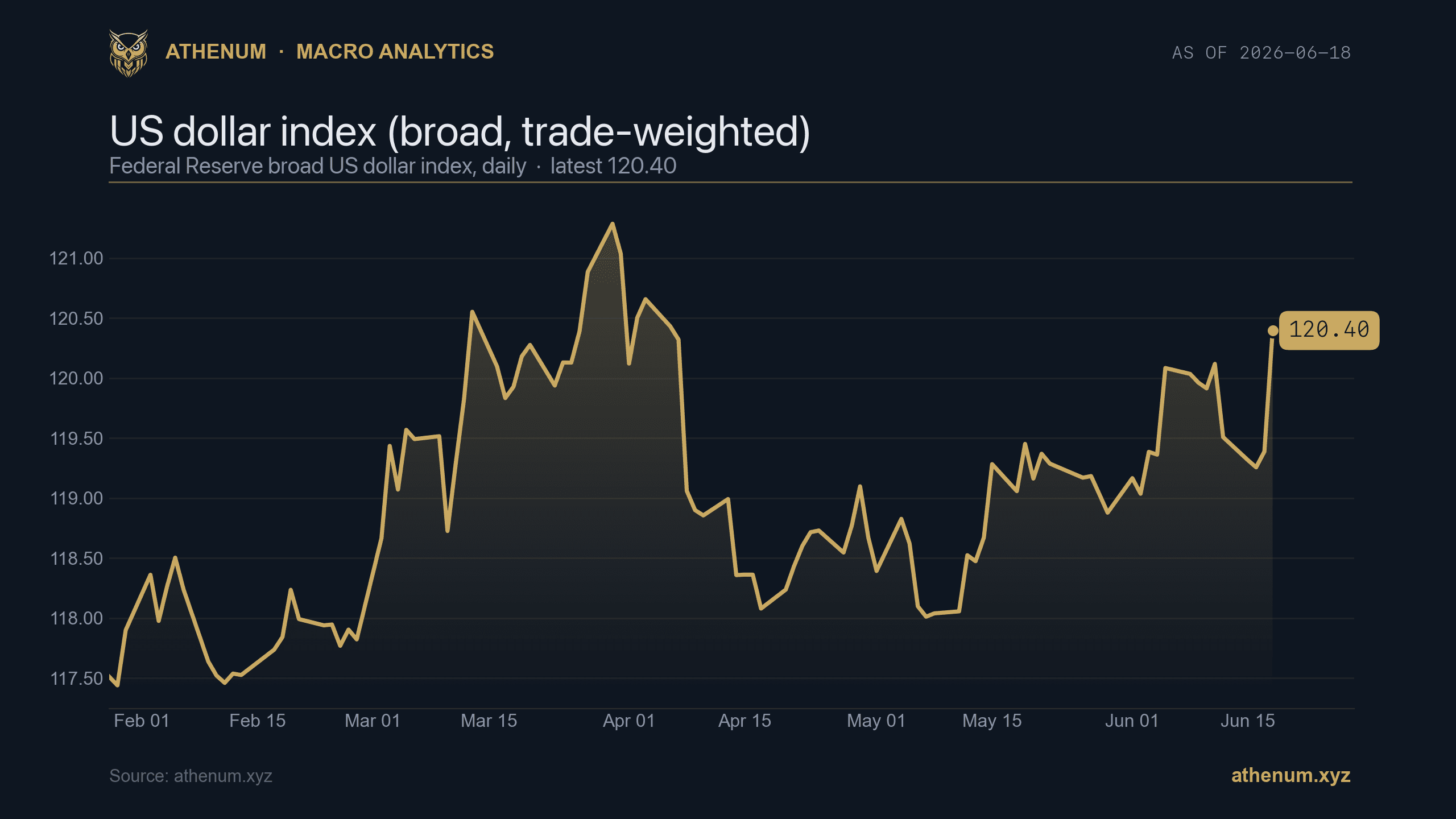

Bitcoin Nasdaq Correlation: How Closely Crypto Tracks Tech Stocks in 2026

Bitcoin now trades as a high-beta version of the Nasdaq. Read the live correlation with first-party data: Nasdaq 26,214, VIX near 17, BTC $59,260, DVOL 43.4.

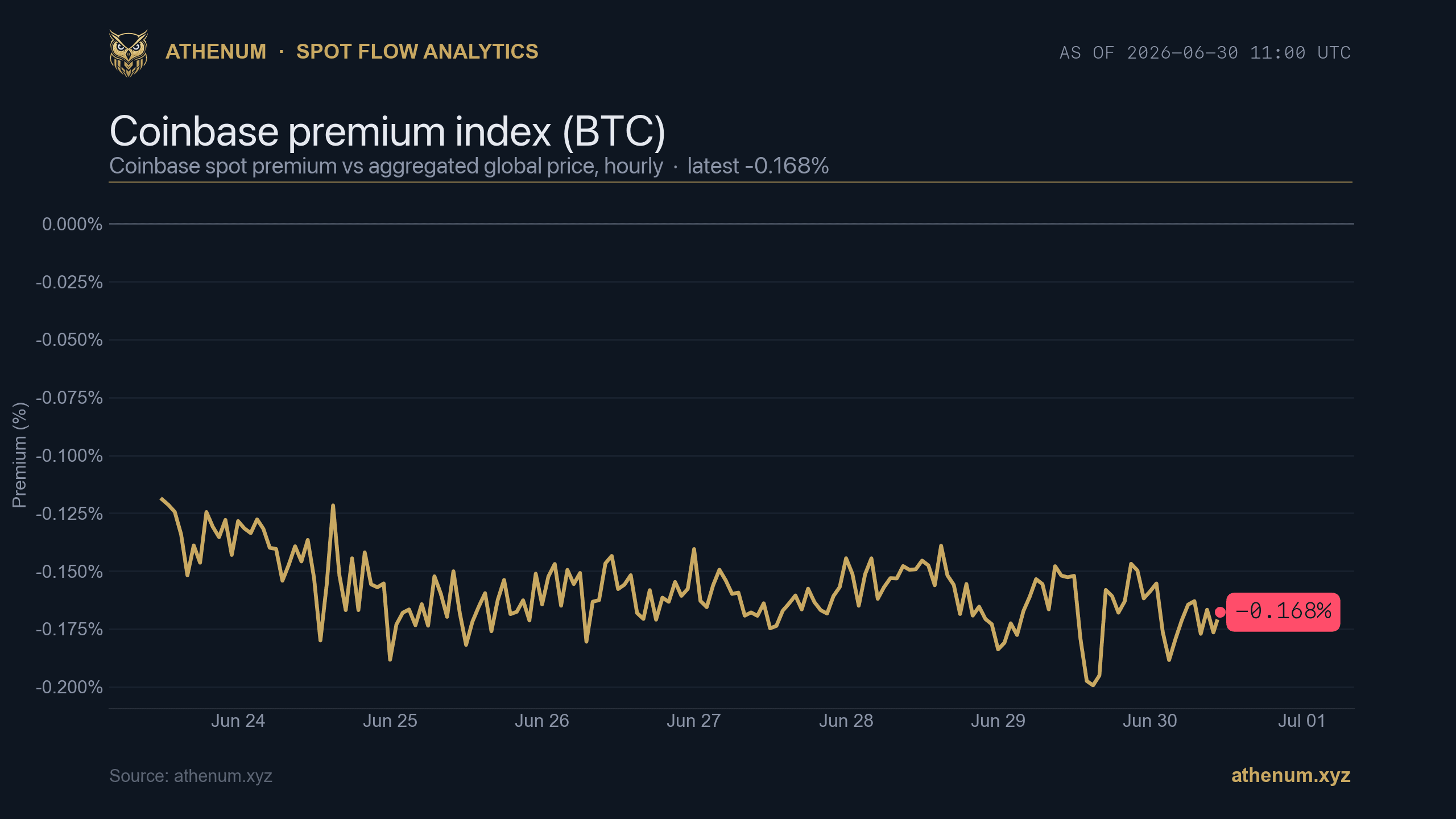

Coinbase Premium Index: Weak US Spot Demand vs Crowded Longs (2026-06-30)

BTC's Coinbase Premium Index sits at -0.168% and was negative in 100% of hourly prints this week, yet the long/short account ratio is 2.04 and funding is +9.68% APR. Here is why soft US spot under crowded leverage is a fragile setup, not a buy signal.

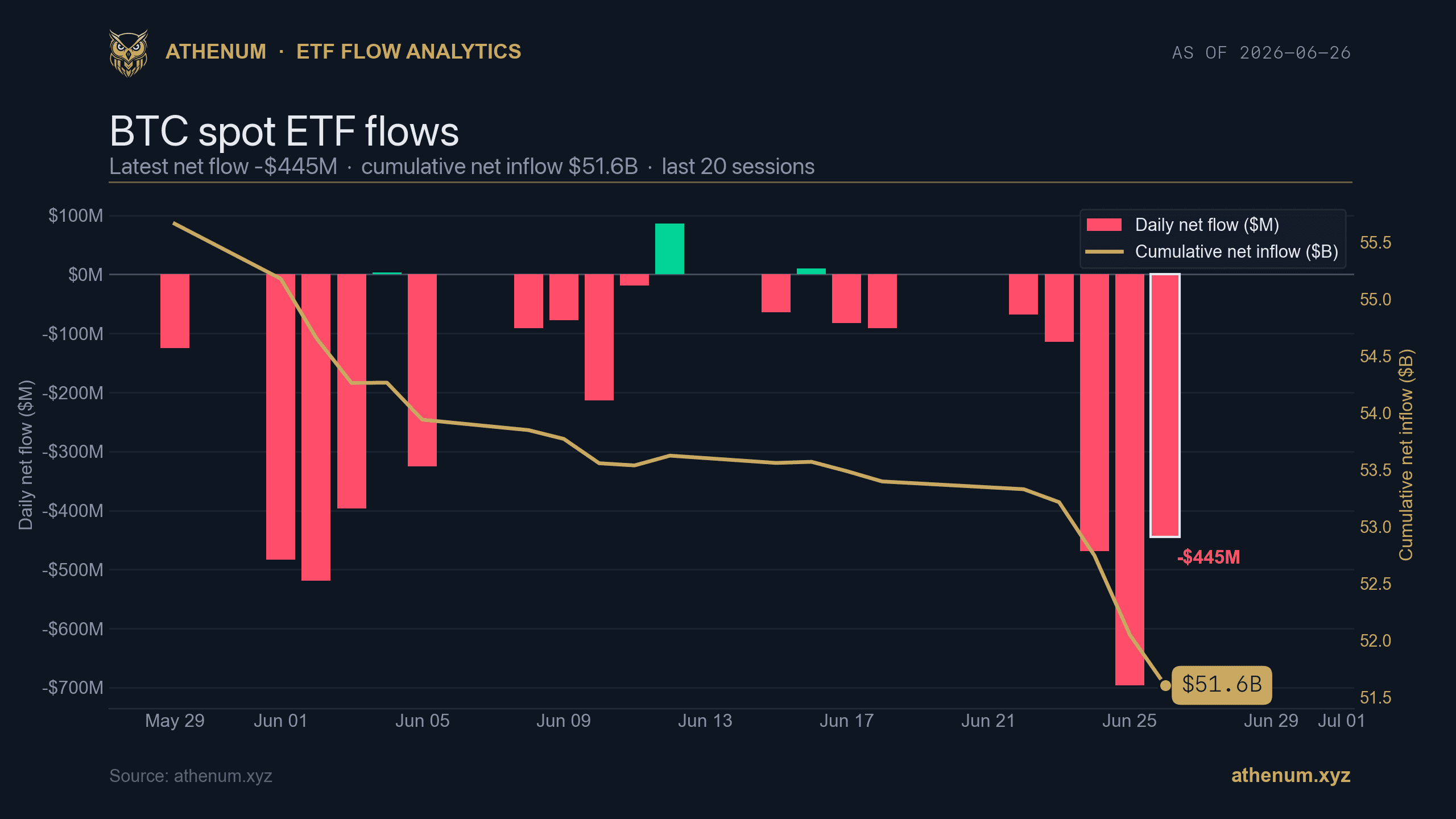

Spot Bitcoin and Ether ETF Flows: Reading the Daily Number Against the Cumulative Base

A spot ETF flow number comes in two forms that get confused constantly: the volatile daily net flow and the slow cumulative base. On 2026-06-26 the Bitcoin funds saw a $445M daily outflow against a $51.6B cumulative base, ETH a $13M outflow against $10.9B, while the futures curve held a calm +4.0% contango. Here is how to read daily against cumulative, BTC against ETH, and flows against the carry.

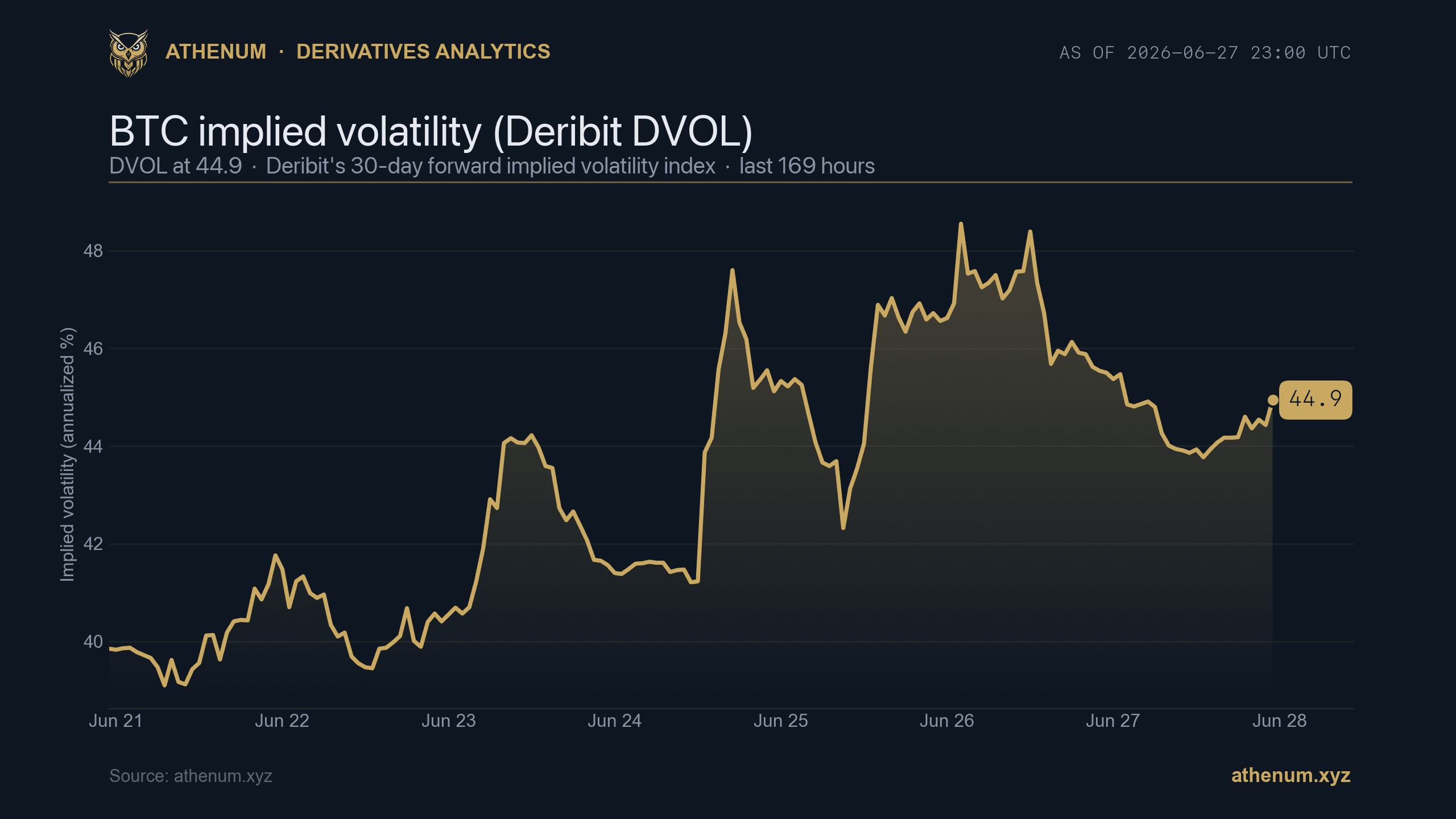

Realized vs Implied Volatility in Crypto Options

Realized volatility is how much price actually moved; implied volatility is how much the options market expects it to move. The gap between them is the volatility risk premium. Here is the distinction, why it matters, and how to read DVOL against positioning, with a live 2026-06-27 read.

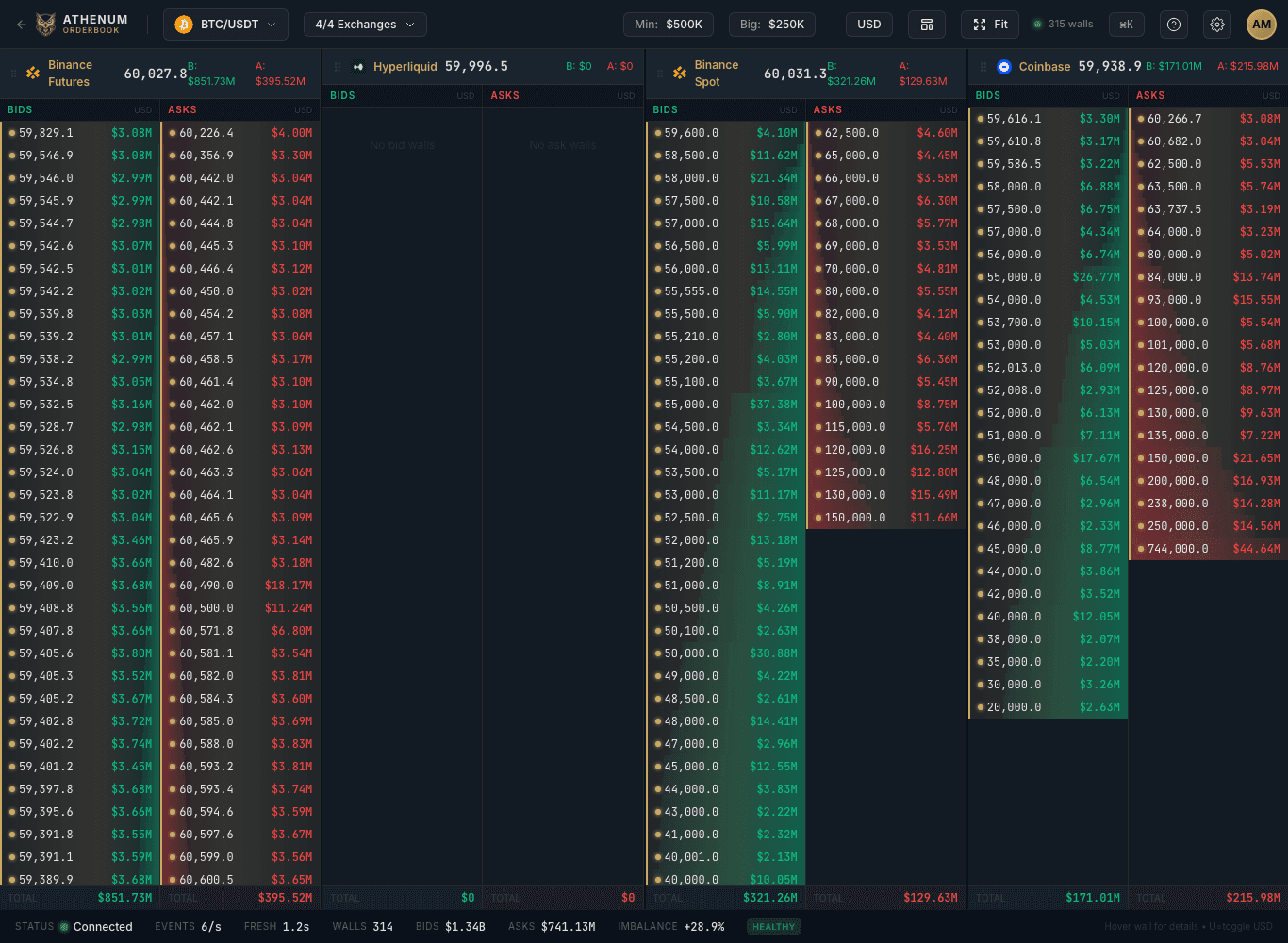

Order Book Imbalance and Liquidity Walls: Why the Number Depends on the Band and the Venue

Order book imbalance compares resting bid and ask liquidity, but a single figure hides where the depth sits. A book can read +28.9% bid-heavy in aggregate and -5.6% ask-heavy at the touch the same minute, and venues disagree. Here is how to read imbalance and liquidity walls across depth bands and exchanges.

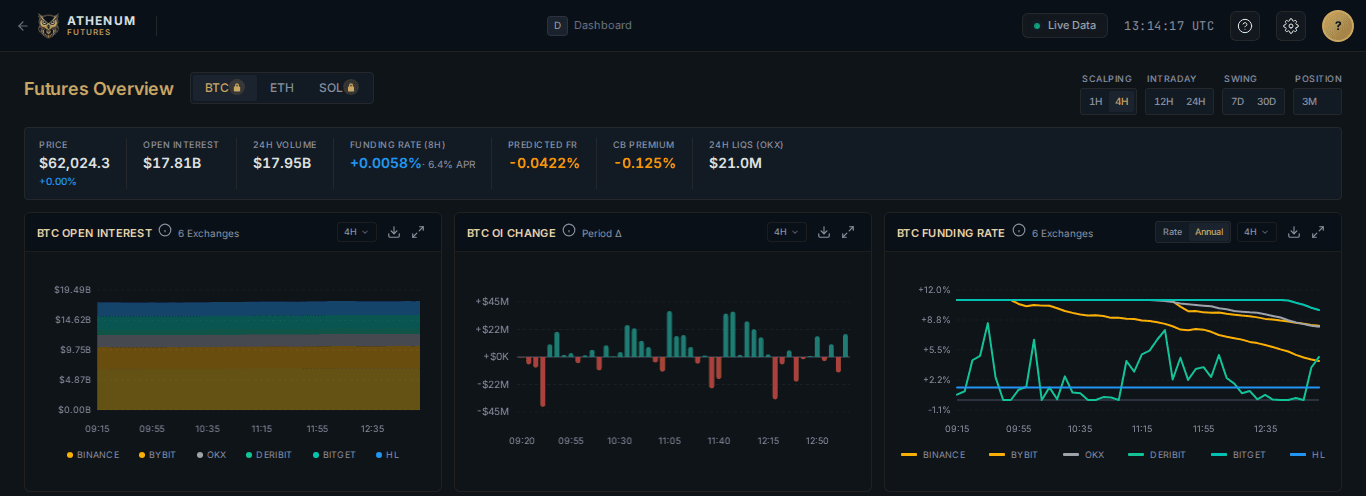

OI-Weighted Funding Rate: Reading One Honest Number Instead of an Average That Lies

A simple average of perpetual funding rates lets a near-empty venue cast the same vote as the deepest book. The open-interest-weighted funding rate weights each venue by its open interest, so the deepest book dominates. Here is what it is, why a flat average lies, the four-step methodology, and how to read it live on Athenum.