TL;DR: A perpetual funding rate is the periodic payment that tethers a perp's price to spot, and reading it off a single exchange can mislead you because a thin venue can print extreme funding that does not represent the market. An open-interest-weighted (OI-weighted) funding rate fixes this by weighting each venue's funding by its open interest, so the aggregate is dominated by where the leverage actually sits. Use it as a positioning gauge, not a timing signal.

What is a perpetual funding rate?

A perpetual future has no expiry, so it cannot rely on settlement to pull its price back toward spot. Instead it uses funding: a recurring cash flow exchanged directly between traders holding the contract. Most venues settle every eight hours, though several now settle hourly and some use a four-hour interval. It is not a fee paid to the exchange.

The direction is simple. When funding is positive, longs pay shorts; when funding is negative, shorts pay longs. The rate itself is built from a premium index, which measures how far the perp trades from its spot index, plus a small clamped interest component. The mechanism nudges the perp back toward the underlying index. If the perp trades persistently above spot, traders are paying up for long exposure, so funding turns positive and the crowded long side incurs a cost to hold while the short side gets paid. That cost is the incentive that keeps the perpetual anchored to spot without an expiry date.

Why does reading one venue mislead you?

Funding is set per venue, and venues are not the same size. A large, liquid exchange and a thin, illiquid one can both quote a funding rate for the same asset, but only one of them carries meaningful leverage.

The problem is that a small venue can print an extreme funding number off a tiny book. If a thin exchange shows funding several times higher than the rest of the market, that figure tells you about a handful of positions on that one venue, not about how the broader market is leaning. Pull your read from that single quote and you can convince yourself the whole market is dangerously one-sided when it is not, or miss real crowding that is concentrated on the venues you are not watching. A single venue is a sample of one, and in derivatives the sample sizes are wildly unequal.

How does OI-weighting fix it?

Open-interest weighting solves the size problem directly. Instead of averaging every venue equally, you weight each venue's funding rate by its open interest, then sum the weighted parts.

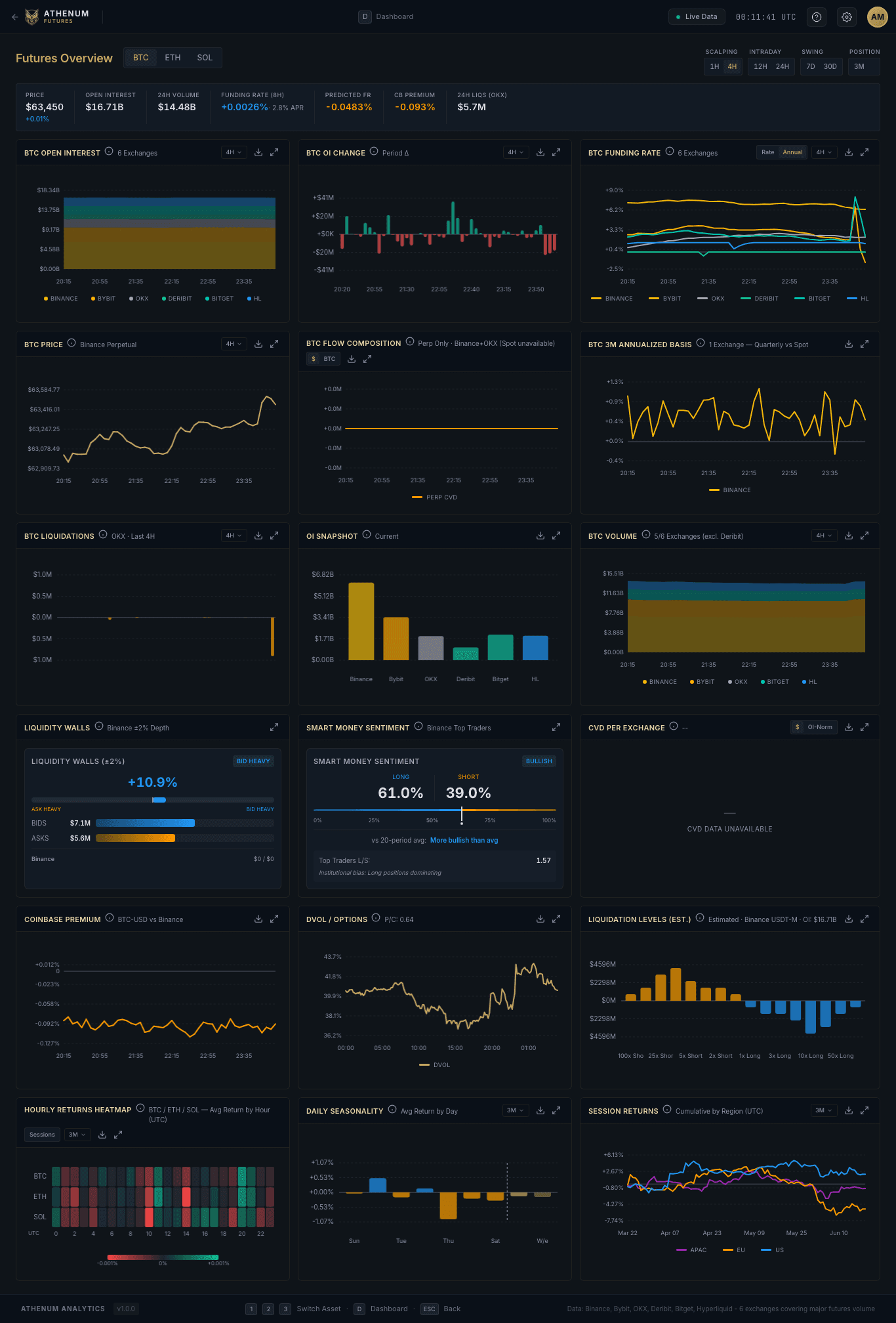

The construction is the one used by aggregated funding indices in the market. Each venue's weight equals its open interest divided by total open interest across all venues, and the aggregate is the sum of (weight x funding rate). A venue holding most of the open interest moves the number a lot; a venue holding almost none barely registers, no matter how extreme its quote. The result is an aggregate that reflects where capital is actually positioned rather than giving a near-empty book the same vote as the deepest market. Data providers such as Coin Metrics and Coinalyze publish OI-weighted aggregated funding for exactly this reason, weighting each venue's funding by its open interest the same way.

How do you read the aggregate?

Treat the OI-weighted funding rate as a positioning gauge. Persistently positive funding means longs are paying to hold, which is the signature of crowded long positioning: the market is leaning long and paying for the privilege. Persistently negative funding means shorts are paying, which points to crowded short positioning.

Magnitude and persistence matter more than a single print. Funding that is mildly positive for weeks describes a steady long bias. Funding that spikes hard and stays there describes leverage piling onto one side, which historically coincides with crowded positioning that can unwind violently. The aggregate is most useful read alongside open interest itself and price: rising price plus rising OI plus climbing positive funding is a different story from rising price on falling OI.

BTC perpetual funding (APR) vs open interest, last 30 days. Source: Athenum.

Where does it still fall short?

OI-weighting removes the thin-venue distortion, but it does not turn funding into a timing signal. Crowded longs can stay crowded and keep paying for a long time before anything breaks, and elevated funding can persist through a trend rather than mark its top. It tells you how the market is positioned, not when that positioning will reverse.

One technical caveat deserves attention: open interest denomination. OI can be reported in the coin (base asset) or in USD, and the two move differently as price moves. Coin-margined and USD-margined markets are often tracked as separate aggregates for this reason. If your weights mix denominations inconsistently, the aggregate drifts, so a clean OI-weighted funding rate normalizes the open-interest basis before weighting.

Athenum aggregates funding rates and open interest across 14 exchanges, so you can read the OI-weighted picture instead of one venue's quote, with liquidations, options and order book depth sitting next to it. The terminal reports the positioning and leaves the trade to you. If you want to try it, the free /tools calculators and a 7-day Pro+ trial (no card) are open.

The takeaway

A perpetual funding rate tells you which side is paying to hold, but only the aggregate tells you the truth at market scale. Weighting funding by open interest across many venues strips out the thin-book noise and surfaces where the leverage actually sits. Read it as a positioning gauge, respect the OI-denomination caveat, and never mistake crowded for about-to-reverse.

One terminal. All the data.

Liquidations, orderbook depth, whale walls & open interest from 4 exchanges, all real-time, in one place.

No credit card required