If you trade or watch crypto derivatives, you have probably seen a single price level mentioned in the days before a big options expiry, often described as the level where price "should" land. That level is the max pain price. It is one of the more misunderstood numbers in options analysis, partly because the name sounds dramatic and partly because people treat a descriptive statistic as if it were a prediction. This piece explains what max pain actually measures, how it is calculated, why some traders believe price drifts toward it, and where the idea breaks down.

What Max Pain Actually Measures

Max pain is the strike price at which the total intrinsic value of all outstanding options for a given expiry is at its minimum for the holders of those options. Said another way, it is the price at which the largest dollar amount of open contracts expires worthless, which is the same as the price at which option writers, the people who sold those contracts, keep the most premium.

The name comes from the buyer's perspective. At the max pain strike, the combined payout owed to call buyers and put buyers across every strike is as small as it can be. Calls that finish below their strike are worthless, and puts that finish above their strike are worthless. The strike that maximizes the total of those worthless contracts is the point of maximum financial "pain" for the option-buying side, and the mirror image of maximum benefit for the option-selling side.

Max pain is defined per expiry. Each weekly, monthly, or quarterly expiration has its own max pain level, because each has its own set of open contracts. A max pain number is meaningless without the expiry it belongs to.

How It Is Computed From Open Interest

Max pain is derived entirely from open interest, which is the count of contracts currently outstanding at each strike. It does not use price history, volatility, or any forecast. It is arithmetic over the current open positions.

The procedure is straightforward in concept. For every strike that has open interest, you treat that strike as a hypothetical settlement price and compute the total intrinsic value that all outstanding options would carry if the underlying settled there. At that candidate price, every call with a lower strike has intrinsic value equal to the settlement price minus the strike, multiplied by its open interest. Every put with a higher strike has intrinsic value equal to the strike minus the settlement price, multiplied by its open interest. Sum the call side and the put side to get the total payout owed at that candidate price.

Repeat that across all candidate strikes, and the strike that produces the smallest total payout to holders is the max pain price. An options dashboard does this sweep automatically and updates it as open interest changes, which it does continuously until the expiry locks. The distribution of open interest across strikes, not the headline total, is what sets the level.

The Theory: Why Price Sometimes Gravitates Toward It

The max pain hypothesis is the idea that, as expiry approaches, the underlying price tends to drift toward the max pain strike. The usual reasoning rests on hedging behavior. Market makers who have sold options hedge their exposure by buying and selling the underlying or related instruments. As expiry nears and time value collapses, that hedging activity can concentrate around the strikes with the most open interest, and the argument is that this flow nudges price toward the level where the most contracts expire worthless.

There is a coherent mechanism here. Delta hedging is real, gamma exposure rises sharply near expiry, and large concentrated positions can influence short-term flow. So the concept is not pure superstition. It describes a force that genuinely exists in options markets.

The Honest Caveat

Max pain is a descriptive statistic, not a guarantee, and it should be used as context rather than a signal to trade on its own. It describes the current state of open interest, which keeps changing, so a level quoted days before expiry can shift meaningfully by settlement.

The pull toward max pain, where it exists at all, is a weak and short-horizon tendency, strongest only very close to expiry when time value is nearly gone. It is not a directional forecast for the days leading up to that point. It is also weak in strongly trending markets. When a powerful directional move is underway, driven by spot demand, macro news, or a liquidity event, that flow easily overwhelms any gentle pull from options positioning. Treat max pain as one input that is more relevant in quiet, range-bound conditions and largely irrelevant in a strong trend.

A Complementary Read: The Put/Call Open-Interest Ratio

Because max pain is built from open interest, it pairs naturally with the put/call open-interest ratio, which divides total put open interest by total call open interest for an expiry or across all expiries. A ratio above one means more outstanding puts than calls, often read as a more defensive or bearish lean, while a ratio below one means more calls, often read as a more bullish lean. Like max pain, it is a sentiment snapshot, not a prediction, and extreme readings are sometimes interpreted contrarily. The max pain strike tells you where positioning is concentrated, and the put/call ratio tells you which side of the book is heavier.

Putting It to Work

The practical takeaway is modest, and that is the point. Max pain marks the price where option sellers are best off and buyers are worst off for a specific expiry, computed cleanly from open interest. Watch it as one piece of the positioning picture, give it more weight in calm markets and near expiry, and discount it when a real trend is running.

To watch open interest, funding, liquidations, order flow, and options positioning update across 14 exchanges, sub-second, start free with no card and a 7-day Pro+ trial. The full real-time read across 14 exchanges is on the Pro+ trial; the free tier is currently delayed and limited.

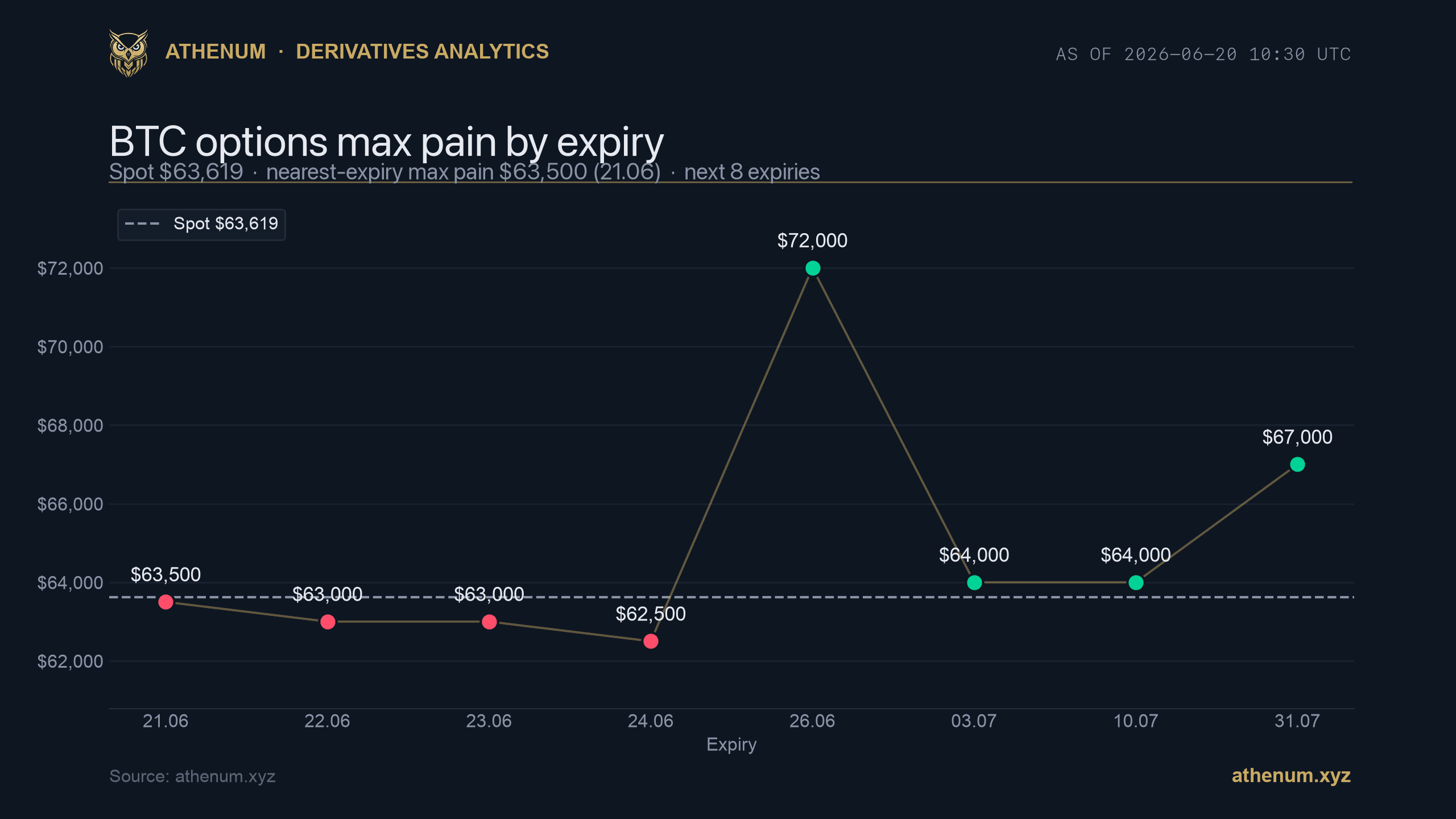

BTC options max pain by expiry vs spot. Source: Athenum.

One terminal. All the data.

Liquidations, orderbook depth, whale walls & open interest from 4 exchanges, all real-time, in one place.

No credit card required